America 2040: The rent is too damn high

The government should sponsor 3% mortgages

[AI generated image]

Key takeaways

1. Housing prices have skyrocketed after the pandemic

2. The federal government should offer low-interest (3%) mortgages to tackle the current housing affordability crisis

3. Selling "America bonds" to investors enables 3% mortgages

4. Zero-interest mortgages should be offered to families with multiple children to counter the declining birthrate

In the midst of the Civil War, Abraham Lincoln signed the Homestead Act of 1862, which granted US citizens free 160-acre plots if they settled and improved the land. The act facilitated the population of the West and the transformation of the US into a continental superpower. During the depths of the Great Depression, FDR passed several programs as a part of the New Deal to make housing more accessible, including creating federally subsidized low-interest mortgages.

Today, housing costs have exploded and homeownership, the traditional route to the American Dream, is out of reach for many Americans. It is taboo to suggest federal government intervention into the free housing market, despite the federal government having done exactly that in the past. These interventions have been extremely effective and are now part of the American mythos. It is time for more government assistance in housing because the rent is too damn high and the birthrate is too damn low. In this post, Ad Astra will propose a policy to offer low-interest mortgages and spur Baby Boom II.

Figure 1: Housing affordability has declined in America

Housing costs have skyrocketed

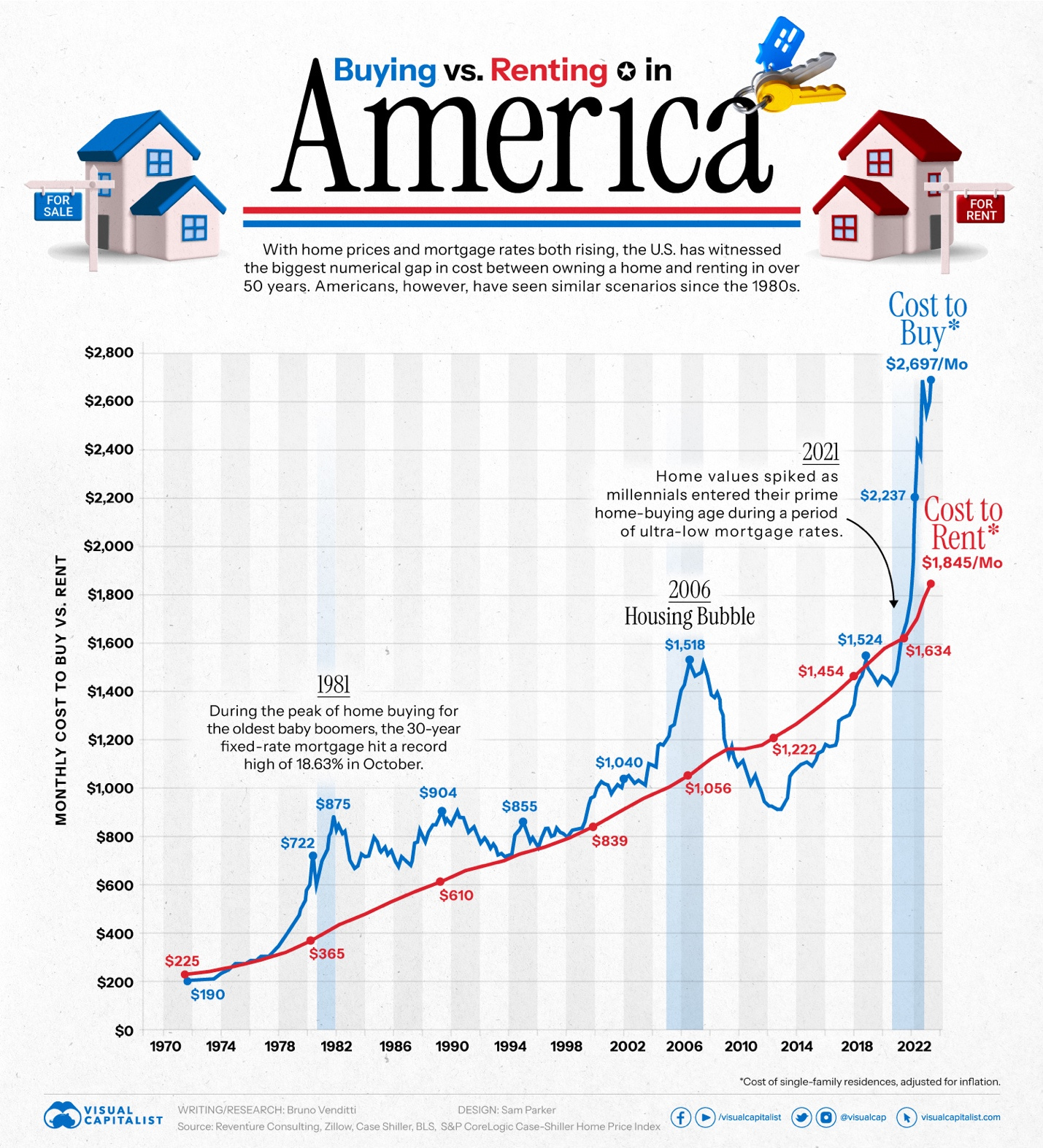

Coming out of the pandemic, US housing costs exploded. Two factors are responsible: 1) higher interest rates and 2) a housing supply shortage. First, as discussed in the previous article, interest rates increased from near zero to higher levels, adding approximately $1100 per month to average mortgage payments. Secondly, the supply of new homes has lagged population growth, especially as Millennials enter their prime home buying age and increase the demand for homes.

Figure 2: Costs of renting and buying a house

The American Dream, cancelled

The ability of anyone, regardless of their station, to succeed in America is a core element of the national lore. One proven way to gain wealth is to own a home, building equity over time. With housing prices exploding, owning a home is out of reach for many young Americans. In particular, the Millennials, buffeted by the Great Recession and student debt, own fewer homes than prior generations. The homeownership rate for Millennials was 51.5% in 2022, compared to 56.5% for baby boomers in 1990 and 58.2% for Gen X in 2006.[i] Home ownership is similar to a first job: it’s the first rung of a ladder that if missed, can derail accumulating wealth. The government must restore the American Dream for everyone by making homeownership more affordable.

America bonds

During WW2, the US government sold the public “war bonds” to fund the war effort. Today, the federal government can offer 3% mortgages to new homebuyers by selling what Ad Astra terms “America bonds”. The market rate for a mortgage today is 8%[ii]. The way it would work is by selling these income and inheritance tax-exempt bonds to investors, who would profit from the interest payments. The investor’s cash would be used to fund mortgages. A prospective homebuyer would apply to a federally guaranteed 3% mortgage secured by the investor’s cash. The homeowner’s interest payments would then go to pay the investor’s interest payments.

Interest payments on standard treasury bonds are taxed as ordinary income so a 3% tax-exempt rate is preferable after-tax to many treasury bonds today (ten-year bills yielding 4.5% in November 2023). Furthermore, inheritance gifts are presently taxed and “America bonds” would be a great way for wealthy Boomers to pass along their wealth to the next generation in a tax efficient way.

It sounds complicated but the key is that “America bonds” would be very attractive to investors and enable homebuyers to access 3% mortgages. A win-win.

Figure 3: America bonds explained

Baby boom II

As discussed in the previous article, America’s birthrate has cratered in the 21st century, threatening the labor supply, pensions, and more by 2040. To address economic barriers to child raising, promote healthy families, and sow the seeds for a second baby boom, the federal government should offer zero-interest mortgages to families with two or more children. Doing so would cost $36 billion per year[iii], less than the $100 billion per year spent on the wars in Ukraine or Afghanistan, and would be more than made up for by the economic benefits of a second baby boom.

Drawing inspiration from historical examples like the Homestead Act and the New Deal, the time is ripe for a modern approach to a growing housing affordability crisis. "America bonds" offer low-interest mortgages and take a step towards reviving the American Dream of homeownership. Moreover, zero-interest mortgages for families with 2+ children address the plummeting birthrate, aligning economic relief with societal growth. It's not just about reducing financial burdens; it's about investing in the nation's future, fostering stable families, and securing a prosperous America for generations to come.

[i] https://www.investopedia.com/millennial-homeownership-still-lagging-behind-previous-generations-7510642

[ii] https://tradingeconomics.com/united-states/mortgage-rate

[iii] Assumptions: $400k avg home value, 8% interest rate, 2.5 million marriages a year, 50% have 2 kids, 30% contingency factor, https://chat.openai.com/share/08808e72-37f4-4359-be0b-d50f340eff40