US Industrial Policy: industrial metals

America must reshore steel, aluminum and casting production

Key takeaways

Revitalizing Metals Production: To ensure national defense and competitiveness, America must urgently reshore the production of crucial industrial metals like steel, aluminum, along with casting and forging processes. The Defense Production Act can provide the legal framework and precedent for rebuilding these vital industries.

Addressing the Production Gap with Foreign Adversaries: Faced with the stark reality that China significantly outpaces the US in steel and aluminum production, strategic investments, tax credits, and interest-free loans are essential to revitalize the domestic metals industry. This approach will not only enhance the US defense capabilities but also stimulate job creation and economic growth.

Forging a Comprehensive Industrial Policy: A robust 21st-century industrial policy, guided by coordination between the Executive Branch, the Defense Department, and Congress, is critical for the US to regain its footing in essential metals manufacturing. By fostering a thriving industrial ecosystem around steel, aluminum, casting, and forging, the US can secure its future in global leadership and defense.

US Industrial Policy Series

1. Overview

2. Metals (this article)

From the late 1940s until 1991, the US was engaged in superpower competition with the Soviet Union. Over those 5 decades, the federal government actively monitored and shaped the industrial base using the Defense Production Act (DPA). Passed at the onset of the Korean War, the DPA authorizes the US President to do three things: 1) require businesses to accept and prioritize contracts for materials deemed necessary for national defense, regardless of a loss incurred on business, 2) establish mechanisms to allocate materials, services, and facilities to promote national defense, 3) control the civilian economy to ensure scarce and critical materials necessary for the national defense effort are available for defense needs.[i]

The DPA played a vital role in the establishment of the domestic aluminum and titanium industries in the 1950s. The government provided capital, interest-free loans, and directed resources to these two industries. The DPA was also used in the 1950s to ensure that government-funded industries were geographically dispersed across the United States to prevent the industrial base from being destroyed by a single nuclear attack.[ii] During the late 1960s and early 1970s, the DPA was used to diversify the US energy mix by funding the trans-Alaskan pipeline, synthetic fuels, and research into LNG.[iii]

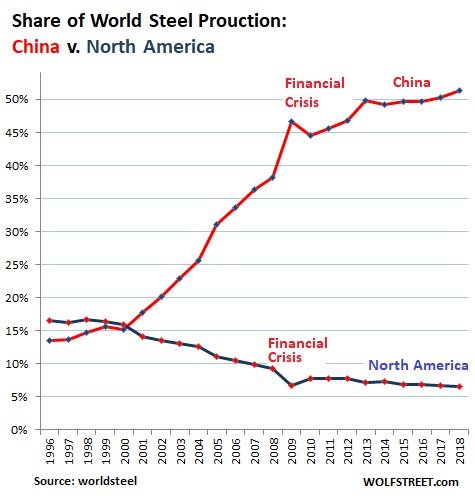

The US won the Cold War, partly thanks to the ability of the industrial base to outproduce the Soviet Union. Today, the US faces a more formidable competitor than the Soviet Union in China but the massive industrial base that won the Cold War has been allowed to atrophy. In the case of steel and aluminum, the raw materials for tanks, ships, and other weapons of war, China produces 12x and 40x more than the US, respectively. In many cases, China is a source for these metals, something that would obviously be untenable in the event of a war.

Figure 1: China vs North America steel production

The DPA provides the legal tool and historical precedent to rebuild the steel and aluminum industries. Along with castings foundries and the derivative processes from these product lines, the President and Congress should use the DPA to rebuild the domestic metals industry in the US.

Steel

The decline of the US steel industry was a complex process that occurred over several decades due to a combination of factors, but greatly accelerated in the 1970s due to rising energy costs from the oil shocks. In addition, the rise of steel production in other countries, particularly in Asia and Europe, led to increased competition for the US steel industry. These countries often had lower labor costs and were able to produce steel less expensively, making it difficult for US producers to compete. The US steel industry was also slow to adopt new technologies and modernize its facilities compared to its international counterparts. This resulted in higher production costs and a decline in competitiveness.

With the US environmental movement peaking in the 1970s, the industry also had to contend with increasingly stringent environmental regulations. Compliance with these regulations added to the operational costs, making US steel more expensive to produce. Key industries that were major consumers of steel, like the US automotive and construction industries, faced their own challenges and declines, which in turn reduced demand for steel.

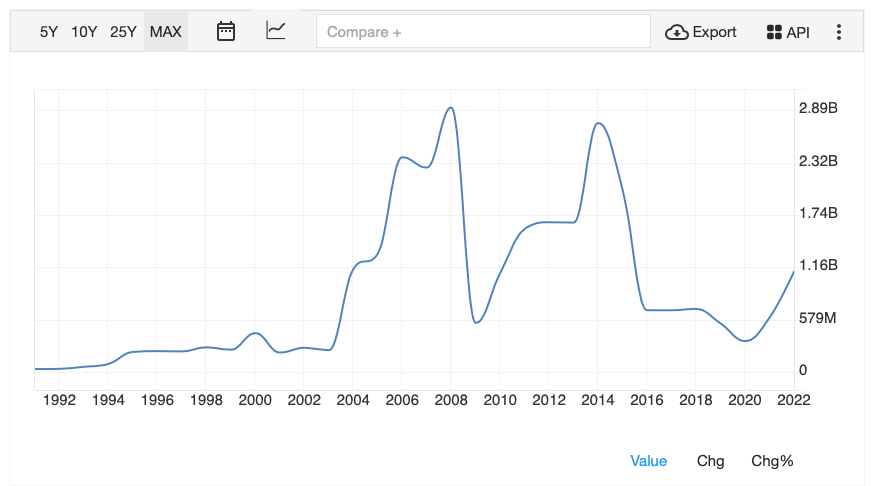

Today, US steel production is down 62% from its peak in 1973 to 86 million metric tons[iv] per year. By contrast, China produces 1,030 million metric tons per year[v], 57% of global steel production. The US imports 29 million metric tons of steel per year[vi], $1.1 billion worth from China[vii].

Figure 2: US steel imports ($) from China[viii]

In 2023, foreign control of the US steel industry continues, as evidenced by Nippon’s (a Japanese company) recent $15 billion bid for US Steel[ix]. Federal regulators (CFIUS) should block this acquisition.

Steel is an incredibly versatile material and has a wide array of applications due to its strength, durability, and cost-effectiveness. Steel plays a particularly critical role in warfighting and national security.

Aluminum

The US aluminum industry followed a similar trajectory to the US steel industry and its decline shares many of the same causes.

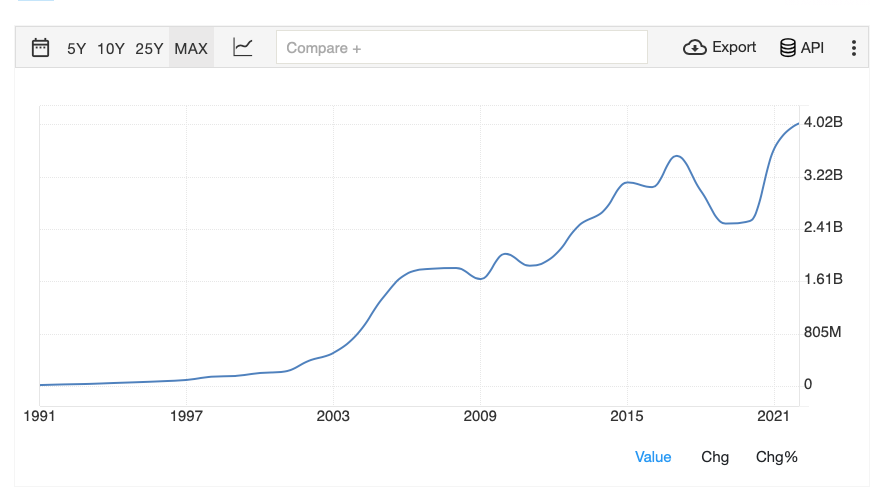

Today, US aluminum production is down 81% from its peak in 1980 to 0.86 million metric tons per year[x]. By contrast, China produces 40 million metric tons per year[xi], 58% of global production. The US imports 5.9 million metric tons of aluminum per year[xii], $4 billion worth from China[xiii].

Figure 3: US aluminum imports from China ($)[xiv]

Aluminum is a highly versatile metal known for its light weight, strength, and resistance to corrosion. These properties make it suitable for a wide range of applications. Aluminum plays a particularly critical role in warfighting and national security.

Casting and forging

Casting and forging are the processes of pouring liquid metal into molds (casting) or shaping metal parts (forging), such as aircraft engine parts or structural components. The decline of the US casting and forging capacity mirrors the decline of the steel and aluminum industries, complete with the rise of Chinese and Indian competition, offshoring, and a dearth of skilled labor.

Today, casting and forging are crucial steps in artillery shell production which has proved essential in modern warfare. In the case of Ukraine, the US has failed to keep up with massive Russian (and her North Korean supplier) artillery shell production. In the case of Ukraine, this failure could be decisive. Ad Astra wrote about this shortcoming last year:

The obvious solution to all this is to ramp up our defense-industrial base. But according to the AP, that will take 5 years and still be insufficient for Ukraine’s needs:

The Army is spending about $1.5 billion to ramp up production of 155 mm rounds from 14,000 a month before Russia invaded Ukraine to over 85,000 a month by 2028, US Army Undersecretary Gabe Camarillo told a symposium last month. “Already, the US military has given Ukraine more than 1.5 million rounds of 155 mm ammunition, according to Army figures. “But even with higher near-term production rates, the US cannot replenish its stockpile or catch up to the usage pace in Ukraine, where officials estimate that the Ukrainian military is firing 6,000 to 8,000 shells per day. In other words, two days’ worth of shells fired by Ukraine equates to the United States’ monthly pre-war production figure.[xv]

Assuming conservatively that Ukraine uses 6,000 shells per day, that’s 240,000 shells per month or about 3x what the US plans to produce in 2028. That is pathetic. WW2 lasted 4 years and the US mobilized to provide enough equipment to supply itself and its allies around the world. The Pentagon was built in 16 months. As previously mentioned on this Substack, it now takes longer on average to get an environmental permit (5 years) than the total time it took— from start to finish—to build the Hoover Dam. We must place a priority on rebuilding our defense industrial base.

Today, the majority of global casting capacity is in China.

We know from Ukraine that modern wars combine hi-tech drones, AI, and space-based surveillance with lots of WW1-era artillery mass. The US is presently overextended supporting wars in the Middle East and Eastern Europe. If we want to win these wars and have any hope in future ones, we need domestic casting and forging capacity.

21st-century industrial policy

To prevail in 21st-century conflicts, the US needs 20th-century industries like steel, aluminum, casting, and forging. There are a host of derivative manufacturing processes that will accompany these manufacturing industries once they are built. The US needs a diverse metals manufacturing ecosystem.

The Manufacturing Czar and the Defense Department should coordinate on which and how many metals projects are needed to meet trade and security objectives. Congress should provide tax credits and interest-free loans to domestic projects in steel, aluminum, casting, and forging. Broad reductions in the corporate tax rate will help foster a thriving industrial ecosystem around the core metals projects.

The imperative to reshore the production of steel, aluminum, casting, and forging in the United States transcends mere economic revitalization—it is a strategic necessity in maintaining national security and ensuring the country's competitive edge. Drawing on the historical blueprint provided by the Defense Production Act and the successes of mid-20th-century industrial policy, the US must now aggressively apply these lessons to confront the challenges posed by contemporary rivals, particularly China. By leveraging federal capabilities to prioritize, support, and expand domestic metals manufacturing, the US can safeguard its defense capabilities, bolster its industrial base, and provide lots of good, middle-class jobs. This initiative demands a concerted effort from both the executive and legislative branches, alongside robust public-private partnerships, to reestablish the United States as a self-reliant industrial powerhouse capable of leading in the 21st century. The time to act is now, leveraging every tool at our disposal to reforge the backbone of American industry and defense, ensuring a future where the nation remains unassailable and prosperous.

[i] https://en.wikipedia.org/wiki/Defense_Production_Act_of_1950

[ii] https://en.wikipedia.org/wiki/Defense_Production_Act_of_1950

[iii] https://en.wikipedia.org/wiki/Defense_Production_Act_of_1950

[iv] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-iron-steel.pdf

[v] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-iron-steel.pdf

[vi] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-iron-steel.pdf

[vii] https://tradingeconomics.com/united-states/imports/china/iron-steel

[viii] https://tradingeconomics.com/united-states/imports/china/iron-steel

[ix] https://www.reuters.com/markets/deals/japans-nippon-steel-plans-acquire-us-steel-7-bln-nikkei-2023-12-18/

[x] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-aluminum.pdf

[xi] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-aluminum.pdf

[xii] https://pubs.usgs.gov/periodicals/mcs2023/mcs2023-aluminum.pdf

[xiii] https://tradingeconomics.com/united-states/imports/china/aluminum

[xiv] https://tradingeconomics.com/united-states/imports/china/aluminum

[xv] AP